blog

Browsing all posts under blog

50 Emerging Industries in India: 2026 Opportunity Map for Global Brands (And How to Get Paid)

If you’re a global brand, India is no longer a “someday” market, it’s one of the last truly large, fast‑growing consumer markets you can still enter early and meaningfully. Over the coming decades, the population is heading towards roughly 1.6 billion, but what matters more is the 300‑million‑plus Indians who already have the purchasing power to buy global products and subscriptions today. This middle class is not confined to Delhi, Mumbai, and Bengaluru. India’s consumer growth is decentralisi

Stripe for India: What Works, What Doesn’t, and Where Global Merchants Lose Indian Customers

If you already run your global stack on Stripe, India looks deceptively simple: turn on international cards, maybe UPI, and you’re done. In reality, India is now a UPI‑first market running on RBI‑specific rules and a new cross‑border regime (PA‑CB) that Stripe was never designed around. This article is for teams who trust Stripe globally, but are now looking at India seriously - SaaS founders, marketplaces, PSPs, and fintech infrastructure players who want to accept payments from India without

PayGlocal vs EximPe for Foreign Merchants: How Global Companies, PSPs and Fintechs Should Collect INR from India

India is now a market where serious foreign merchants treat “how do we collect INR via UPI and local methods, with offshore settlement, under RBI’s PA‑CB regime?” as a core strategy question, not a side project. PayGlocal and EximPe both sit in this new, regulated layer, the choice between them is less about “is this legal?” and more about whether your India checkout is card‑first or UPI‑first. Why INR collections from India now matter India is one of the fastest‑growing digital economies, wi

Razorpay vs EximPe for Foreign Merchants: PA‑CB Guide to Receiving Payments from India

India has quietly become one of the hardest markets to “get right” for foreign merchants: UPI is now the default way to pay, RBI has introduced a dedicated Payment Aggregator – Cross Border (PA‑CB) licence, and global card‑only setups simply don’t convert well anymore. At the same time, both Razorpay and EximPe now hold RBI PA‑CB authorisation and let foreign businesses collect from Indian customers in INR and settle into overseas bank accounts without a local entity. This article compares Razo

PayPal in India for Foreign Merchants: What Works, What’s Restricted, and Better Alternatives

If you treat India as “just another card market”, you will systematically underestimate how much revenue you can unlock here. UPI has become India’s default way to pay, with reports showing around 500 million users and tens of millions of merchants using it daily. At the same time, India’s cross‑border commerce is growing across SaaS, e‑commerce, digital content and B2B services, which makes “accept payments from India” a real product requirement for global companies, PSPs and fintechs. PayPal

INR Pricing for Global SaaS: Should You Charge Indian Customers in Rupees?

Indian customers are increasingly buying global SaaS and digital products, but many are still forced to pay in USD and absorb FX fees, GST on foreign services, and conversion losses from their INR income. As UPI and other local methods dominate Indian digital payments, the question for global SaaS, PSPs, and fintechs is simple: should you move to INR pricing and if yes, how do you still settle in USD/EUR while staying compliant? Why INR pricing matters now India is now one of the fastest‑grow

Shopify India UPI Payment Integration Guide for Global Stores (Without a Local Entity)

Global Shopify stores can now offer UPI‑first checkout to Indian buyers without setting up an Indian company, by plugging into RBI‑regulated Payment Aggregator – Cross Border (PA‑CB) providers that collect in INR and settle offshore in USD, EUR and other major currencies. India is now one of the world’s largest digital payments markets, with UPI handling well over 80% of all digital transaction volumes and processing more than 170 billion transactions in 2024 alone. For e‑commerce, UPI has beco

Collect Payments from India: The Complete Guide for Global Businesses, PSPs and Fintechs

Accepting payments from India is no longer a “nice to have” for global businesses and PSPs, it’s becoming a core growth channel that now requires a local, UPI‑first, RBI‑compliant strategy. Indian customers increasingly expect to pay in INR via UPI and other local methods, while foreign businesses want settlement offshore in hard currency and a simple way to stay within India’s new Payment Aggregator – Cross Border (PA‑CB) regime. Why accepting payments from India matters now India is one of

The Complete List of RBI PA‑CB Licensees in India (2026): A Practical Guide for Global Companies, PSPs & Fintechs Receiving Payments from India

India’s new Payment Aggregator – Cross Border (PA‑CB) framework has created a regulated “entry door” for global companies, PSPs and fintechs that want to collect money from Indian customers in a compliant way. This blog summarises what PA‑CB licences are, how many licensees exist as of early 2026, who the key players are, and how global firms can plug into these rails. For global companies, PSPs and fintechs that want to collect online payments from Indian customers, only RBI‑authorised PA‑CBs

PA‑CB License: The Complete Guide for Global Payment Companies & PSPs

India‑linked cross‑border payments are scaling fast, and the Reserve Bank of India (RBI, India’s central bank) has responded by directly regulating non‑bank cross‑border payment aggregators through a new Payment Aggregator. Cross Border (PA‑CB) framework. For global PSPs, wallets, marketplaces and SaaS platforms, PA‑CB is now the primary on‑ramp to serve Indian exporters and importers in a clearly regulated way. Why PA‑CB Matters for Global Payment Companies Over the last decade, Indian freel

What is a Payment Gateway? A Beginner’s Guide to Online Payments

With everything going digital, every business that wants to accept online payments should learn about payment gateway technology. As online shopping rapidly gains popularity in countries like India, payment gateways are playing a crucial role in ensuring transactions are both safe and easy to complete. At Eximpe, we believe it’s essential to make the online payment gateway clear, as this is the first step in building trust that helps a business grow. What is a Payment Gateway? A payment gatew

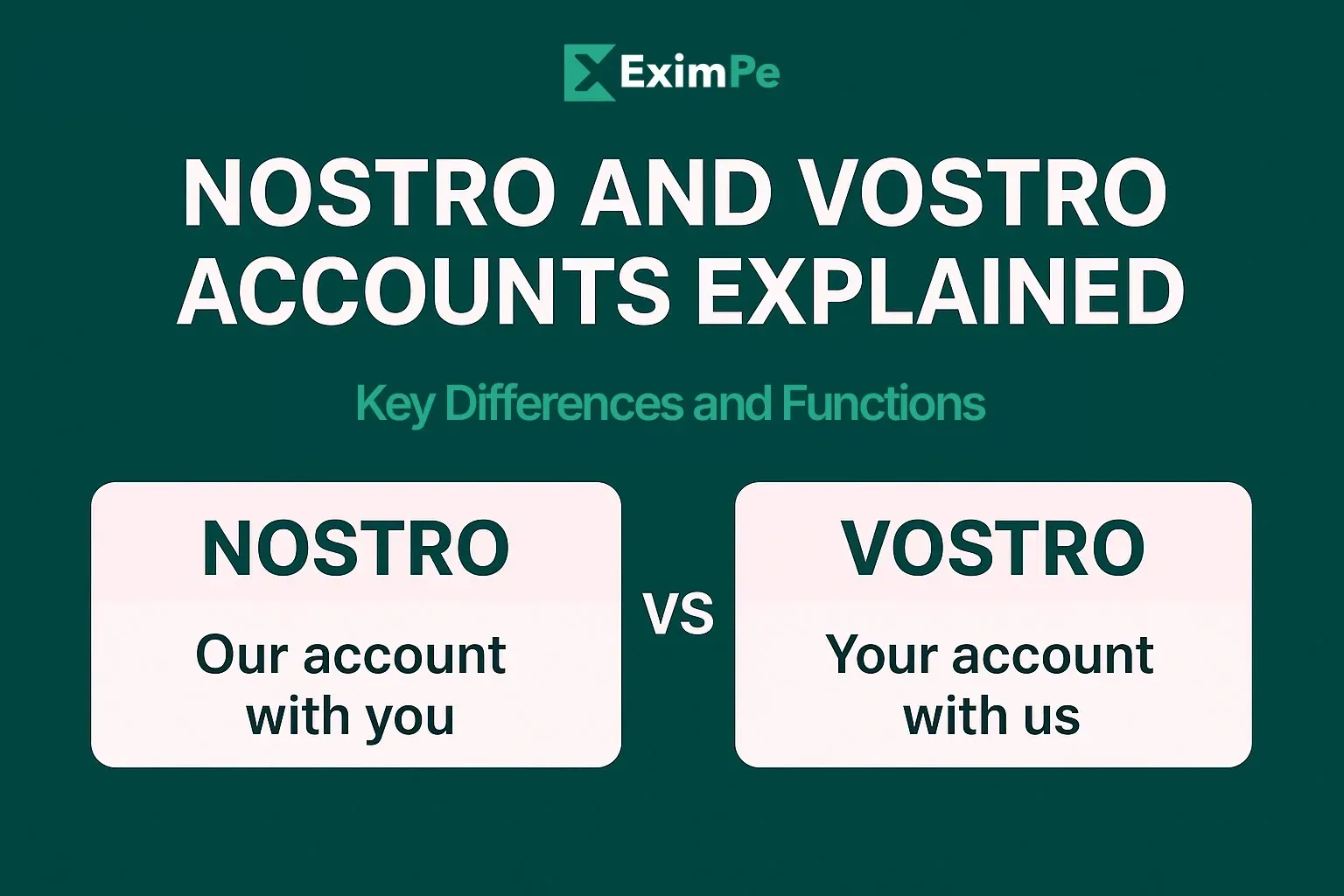

Nostro and Vostro Accounts Explained: Key Differences and Functions

In international banking, two terms frequently appear—Nostro Account and Vostro Account. These accounts play a critical role in facilitating global trade, foreign exchange transactions, and cross-border banking. While both accounts are linked to international financial transactions, they serve different functions and perspectives. This guide explains their meaning, features, differences, and real-world use cases in simple terms. What is a Nostro Account? A Nostro account is an account that a

Simplify Your International Payments

Skip the complexity of traditional wire transfers with EximPe's smart payment solutions

Lightning Fast

Complete international transfers in hours, not days, with real-time tracking

Bank-Grade Security

Multi-layer encryption and compliance with international banking standards

Global Reach

Send payments to 180+ countries with competitive exchange rates

Why Choose EximPe for International Payments?

EximPe Support

How can we help you with your global payments today?

Stay Informed with EximPe News

Subscribe to our newsletter for the latest updates on import-export regulations, market trends, and exclusive insights from industry experts.